This analysis uses key indicators from the Job Openings and Labor Turnover Survey (JOLTS) to investigate how firms are hiring and retaining workers and the implications for the labor market. More recently, a declining quit rate, and lower rates of job openings, separations, and hires, suggest that both workers and firms are behaving with caution. The labor market might be at a turning point.

JOLTS reports, like the monthly Employment Situation report, can provide insight into whether the labor market is expanding at a healthy pace. At the aggregate level, the picture is one of consistent albeit moderating expansion; however, things are more mixed at the industry level. Elevated net hires are concentrated in a few industries, notably construction, health care, and government, while most other industries are experiencing slow growth. While five industries experienced contractions this month, and eight ticked down relative to September, only one industry, durable goods manufacturing, has contracted on average on a year-to-date basis.

Employment continues to grow

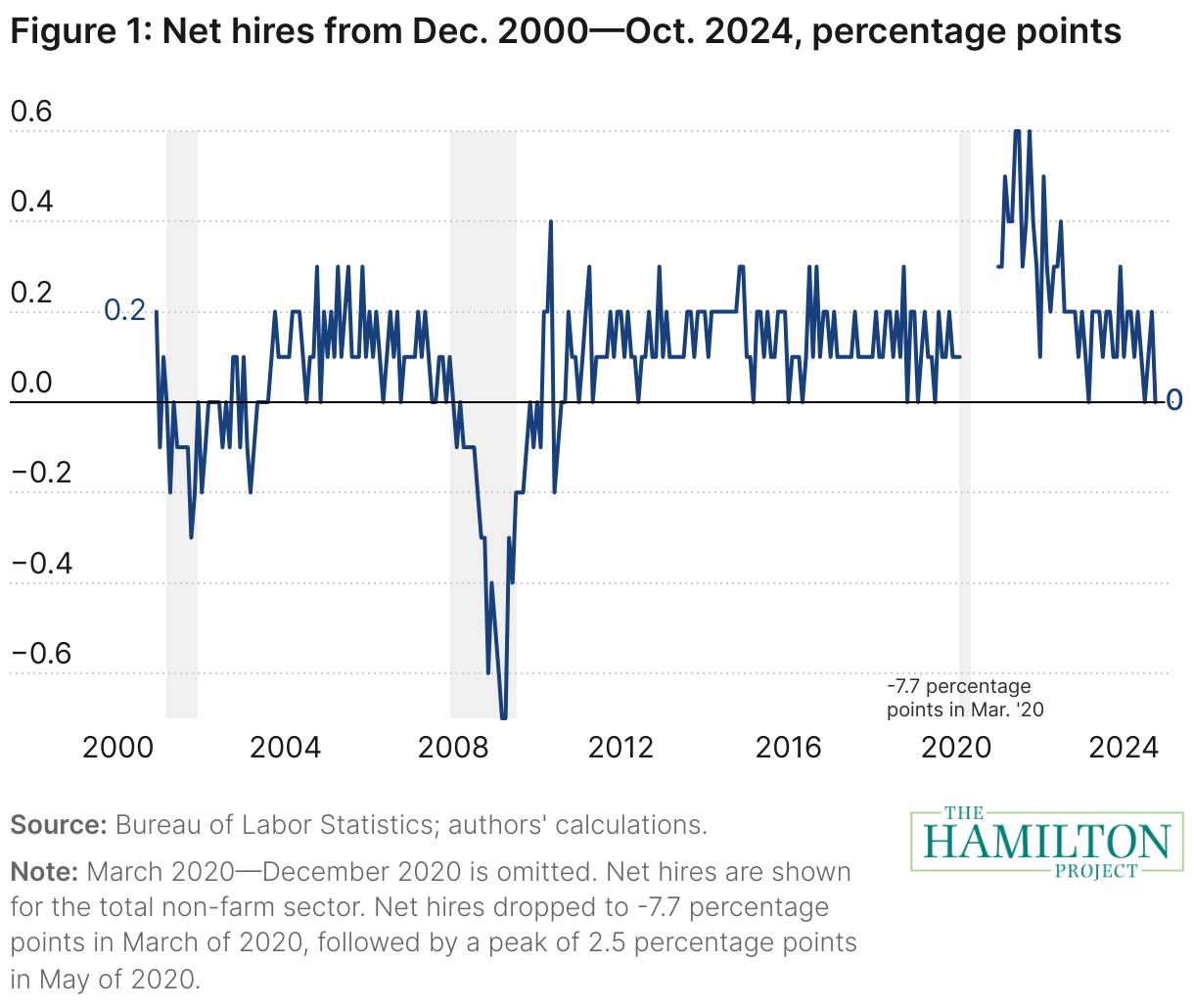

Figure 1 plots the net hire rate—measured as the difference between the total number of hires and separations divided by total employment—for the non-farm sector from December 2000 to October 2024. During the early stages of the pandemic, the net hire rate plunged, driven by a spike in total separations of 11 percent of employment. Starting in May 2020, the net hire rate bounced back over several months with a period of elevated hiring. We omit March to December 2020 from figure 1 to showcase longer-term trends. Since late 2022, the net hire rate has largely matched what it was in the pre-pandemic period, generally in the range of 0 to 0.2 percent of employment.

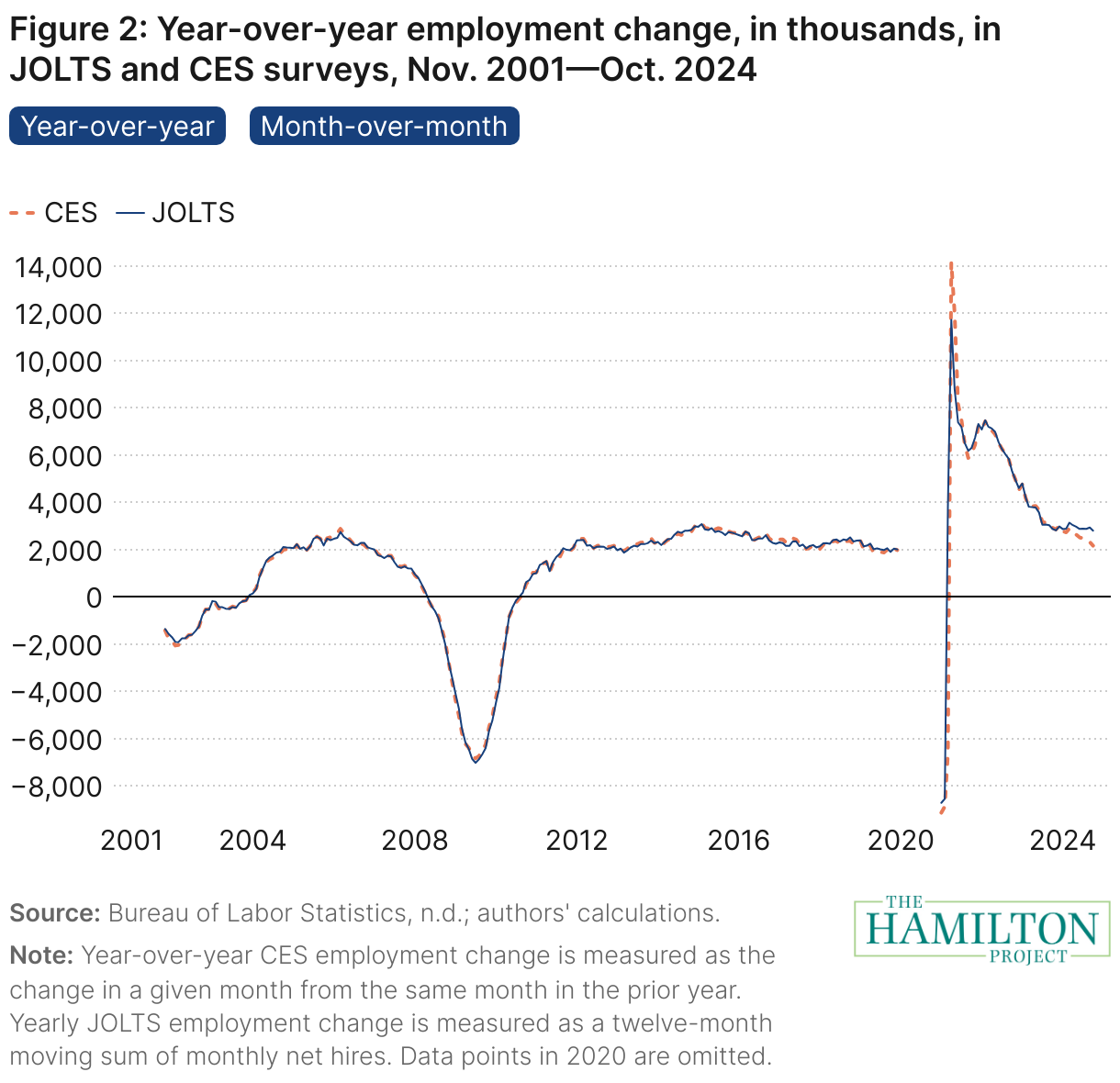

The moderate pace of net hires in the JOLTS data is similar to the recent trends in payroll employment reported in the Establishment Survey. The data interactive in figure 2 shows measures that (for the most part) are directly comparable between the two surveys: month-over-month or year-over-year changes in employment. While month-to-month comparisons reflect some seasonal differences between the surveys, technical adjustments for definitional differences ensure that the two measurements align well over longer time spans. Both JOLTS (released this week) and the Employment Situation report (released last month) show slowing job growth in October. However, observers have noted that both surveys that month were susceptible to temporary negative shocks (labor strikes and hurricanes). The job report scheduled for release tomorrow (December 6) will contain revisions to October’s job estimates as well as new estimates for November; together, these numbers will shed light on whether the apparent slowdown last month is sustained.

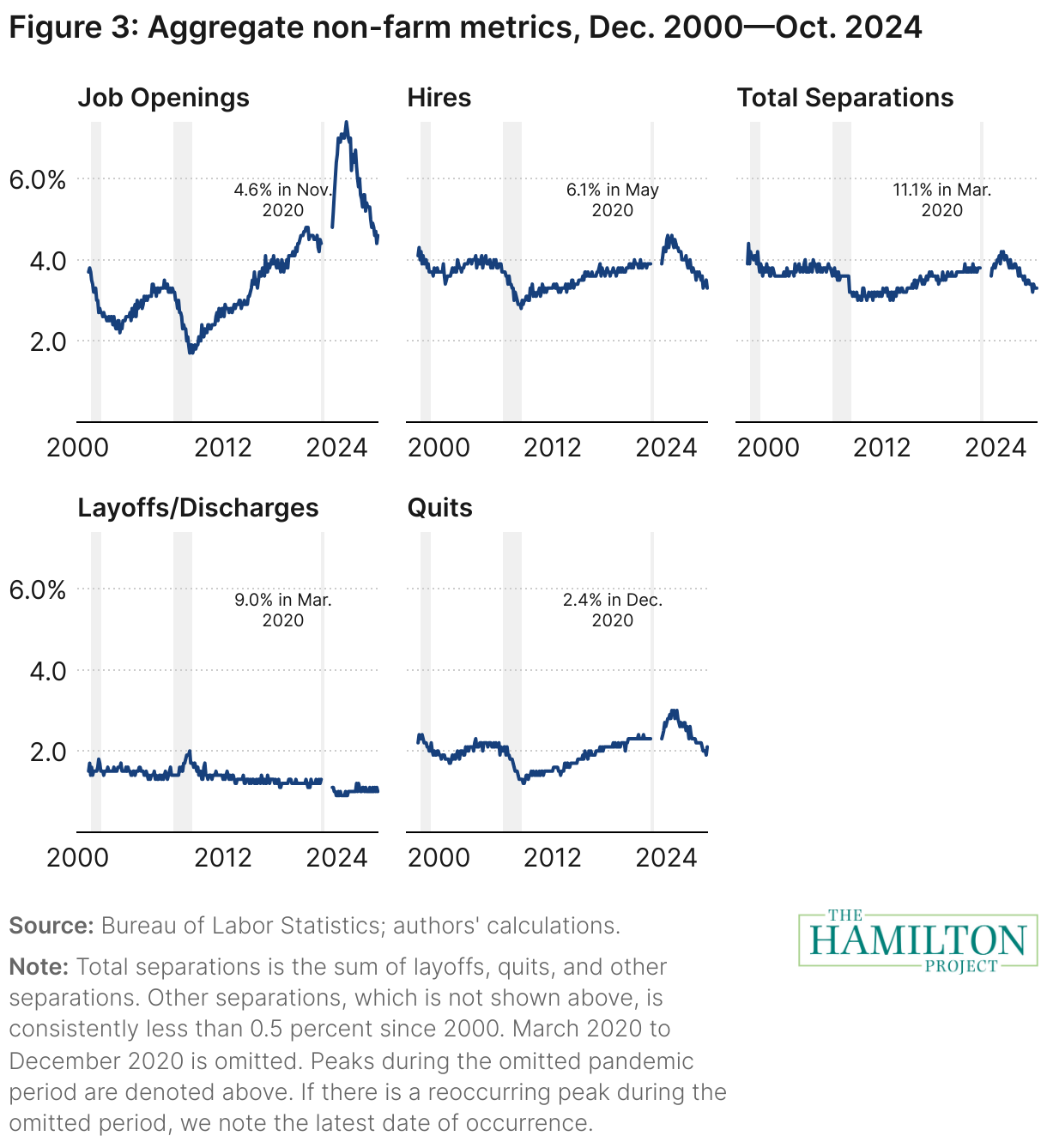

Figure 3 shows rates of job openings, hires, and separations. Both job opening and hire rates have generally been moderating since 2022, although job openings ticked up in October. The figure also shows that, prior to this month, the decline in the total separation rate—which includes quits, layoffs or discharges, and other separations—has been driven primarily by the falling quit rate, as the rates of both layoffs and other separations have remained relatively flat. In general, the quits story since 2022 has been consistent: The labor market is softening and workers are behaving with greater caution. Nonetheless, in October, the quit rate ticked up to 2.1 percent, the first time it has increased in a year and a half. Although the one-month changes in quits and job openings should not be overinterpreted, because people are more likely to quit their jobs when a strong labor market offers plentiful openings, the joint increase in the quit rate and job openings rate in October is notable.

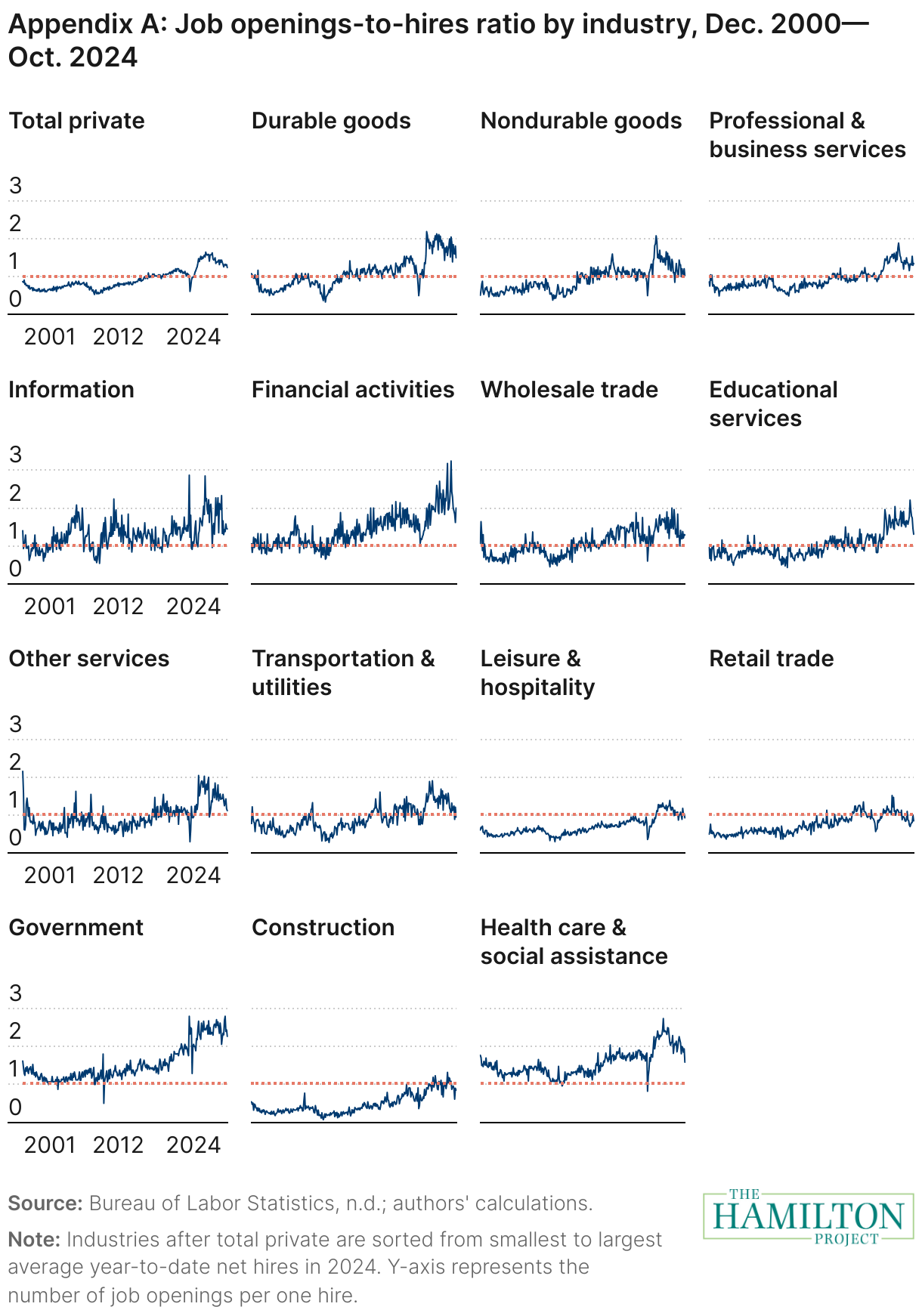

Moving beyond the aggregate, figure 4 plots net hires as well as the hire, quit, and layoff or discharge rates for each industry in turn. We show the aggregate rates as the point of comparison. While subject to greater volatility and industry-specific disruptions, industries have generally followed the private sector’s cyclical contractions and expansions. Each industry generally falls into a category of (1) expansion, outrunning the private sector; (2) slow growth consistent with the private sector as a whole; or (3) pockets of potential concern including indications of contraction.

Indeed, nearly all industries have expanded so far in 2024. Thirteen out of 14 industries have had a positive net hire rate on average in 2024, and four of those have had rates higher than both the private sector average and their respective pre-pandemic benchmarks—health care and social assistance, construction, government, and retail trade. On a year-to-date basis, the average net hire rate was negative in one industry: durables manufacturing. Of the 13 industries that continued to expand, four had negative net hire rates in October—information services, financial activities, professional and business services, and leisure and hospitality. Overall, net hires in eight industries declined in October—six of which were driven by a relative decrease in hires or relative increase in quits, that is, layoffs did not contribute to the decline. Retail trade is the only industry of these eight for which the decline was driven by a jump in layoffs. While health care also saw an uptick in layoffs, its decline in net hires was also driven by an uptick in the quit rate. In year-to-date terms, layoffs appear elevated relative to the pre-pandemic period for four industries: financial activities, manufacturing (both durables and nondurables), and transportation, warehousing, and utilities.

A comparison of hires, quits, and layoffs for two industries—durables manufacturing and health care and social assistance—shows the range of trends across industries. These two industries have seen both hires and quits come down in the last two years. In durables manufacturing, however, average hires from January to October have decreased more than quits over the last two years, while the opposite is true in health care: Average quits have come down faster than hires since 2022. Moreover, while both industries saw declines in the average January to October layoff rate since 2023, the layoff rate in health care and social assistance has decreased by more (and increased by less from 2022 to 2023). This comparison underscores that while the hire rate remains higher than the quit rate across all industries, the relative rate of change for hires versus quits, as well as marginal changes in layoffs, have important implications for the health of the industry. Health care and social assistance continues to expand, while durable manufacturing has experienced no expansion since January of this year.

Select Industry:

Job openings ticked up

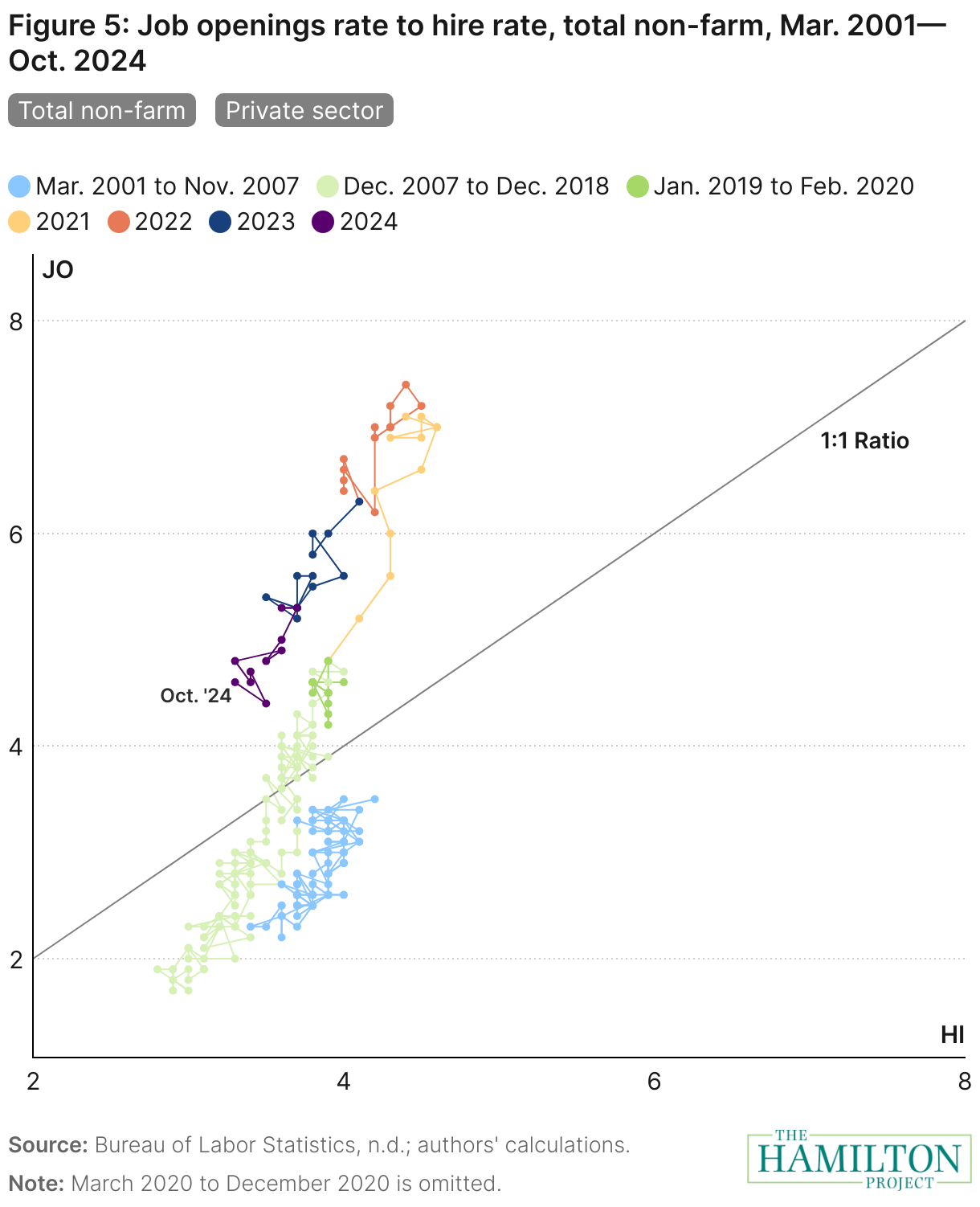

Changes in job openings, often interpreted as changes in labor demand, may reflect several underlying factors. These factors include replacement hiring to counteract separations, how successful firms are in converting job openings into hires, and changes in technology or work practices, such as online meeting software and remote work arrangements. To that end, job openings are best understood in relationship to hiring (openings-to-hires rate ratio, figure 5) and the unemployment rate (Beveridge curve, figure 6).

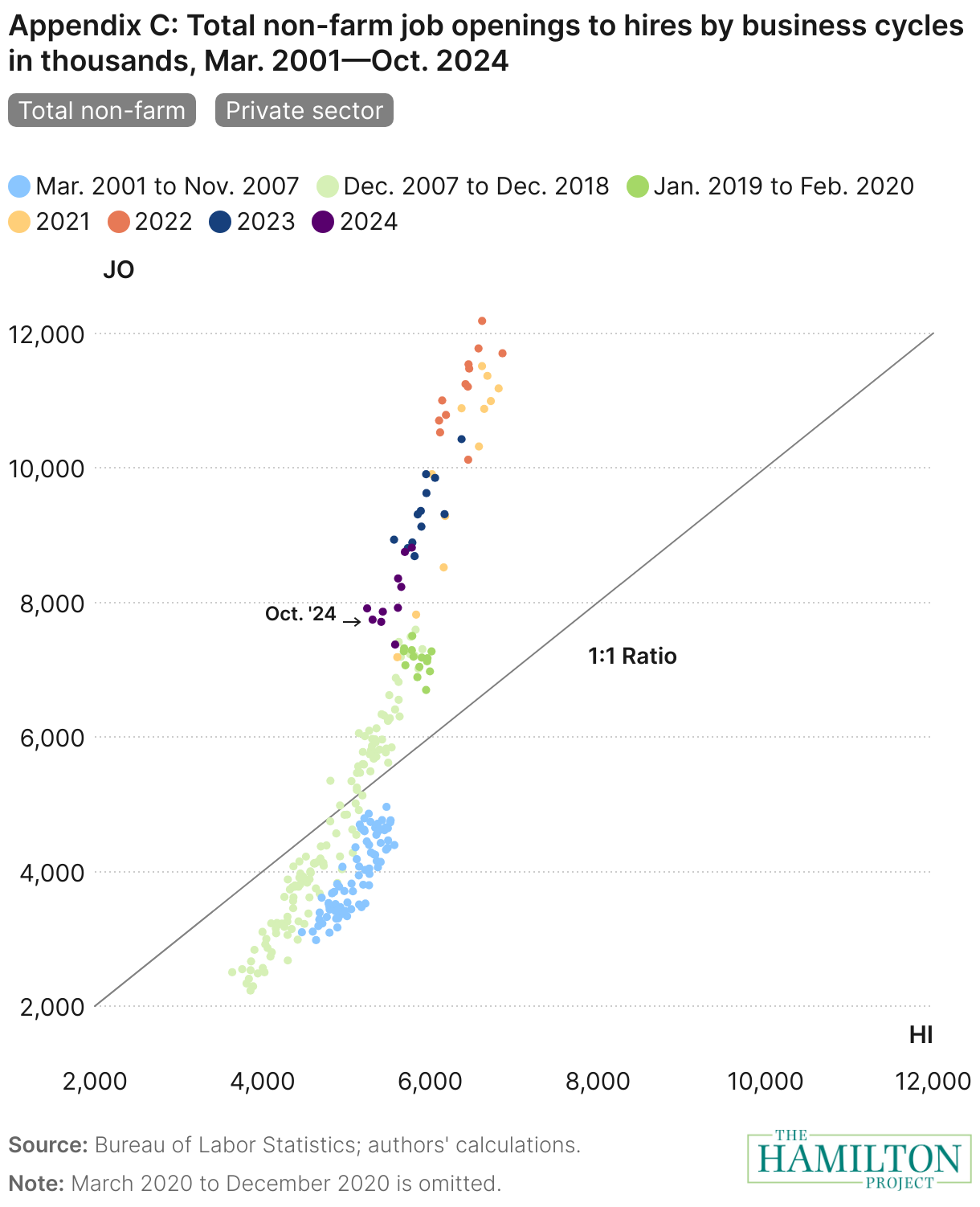

The job openings-to-hires ratio captures the relative ease and efficiency of employers in filling open positions (figure 5, panel A). A ratio above 1 signifies that there are official job openings which firms are unable to fill within 30 days, while a ratio below 1 signifies that there are more hires than official job openings. Industries with a job openings-to-hire ratio greater than one are designated as high need. The job openings-to-hires ratio also helps clarify the degree to which a falling hiring rate suggests less job availability or a lower capacity of firms to fill open positions.

Despite a steady decline in job openings since 2022, the openings-to-hires ratio remains elevated—the current openings-to-hires ratio ticked up this month and remains higher than any given month of 2019. Following a relative decline in the openings-to-hires ratio in September, the job openings rate ticked up in October to 4.6 percent while the hiring rate ticked down to 3.3 percent, constituting a ratio of 1.4. Preceding the pandemic, this same opening rate (4.6 percent) corresponded to a hiring rate of 3.8 to 4.0 percent and a ratio of 1.15 to 1.21.

The elevated openings-to-hires ratio is not driven by the government sector. Even when we focus on the private sector, we observe a similar trend. The openings-to-hire ratio for the private sector in October was 1.33, also higher than any given month in 2019. Moreover, the job openings rate was 4.8 percent relative to a hiring rate of 3.6 percent. A given rate of 4.8 percent pre-pandemic corresponded to a hiring rate of 4.2 to 4.4 percent, or a ratio around 1.1.

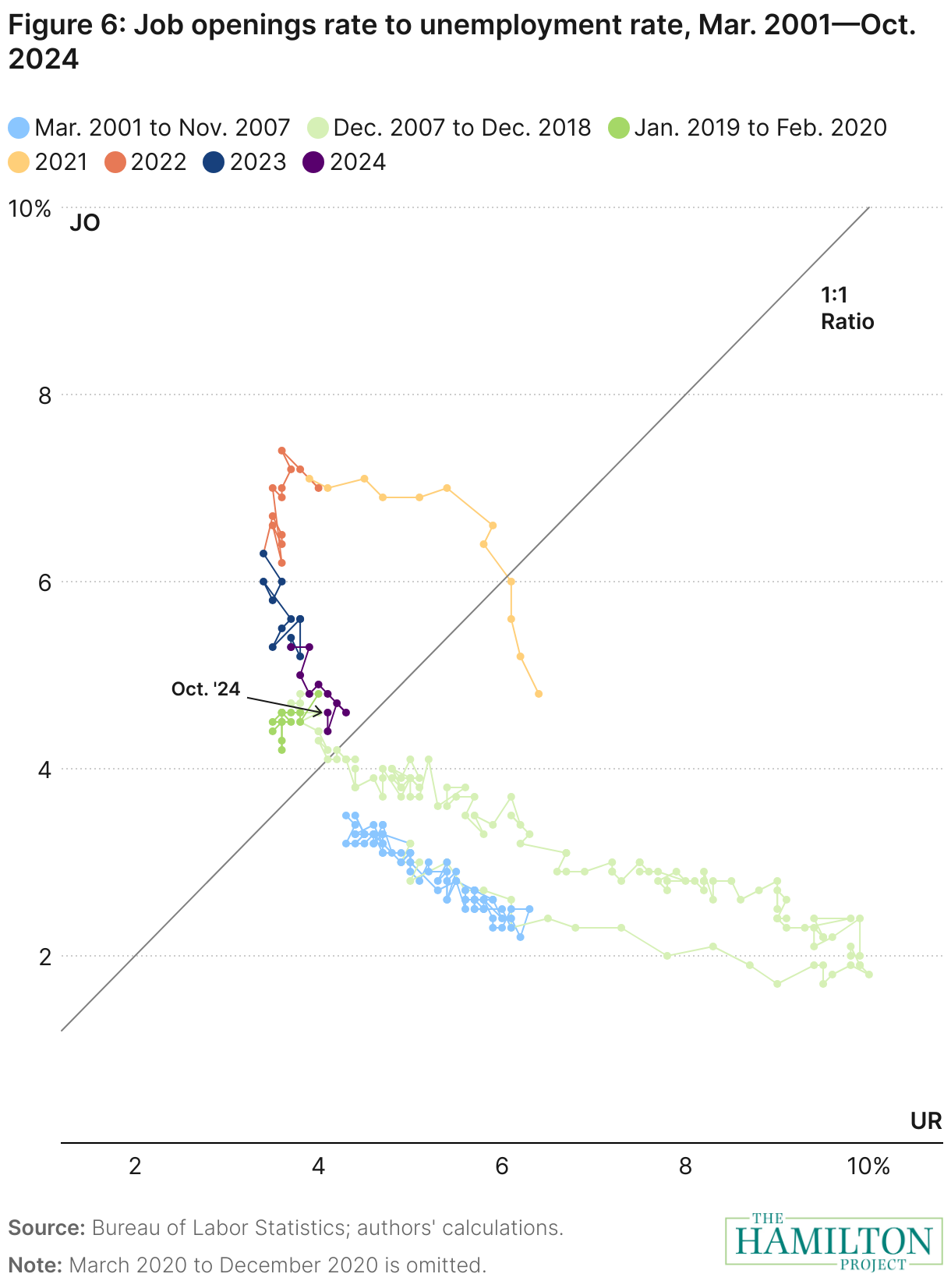

Figure 6 compares the job openings rate to the unemployment rate, also known as the Beveridge curve. It represents another way of illustrating how efficiently the labor market is operating. A job openings-to-unemployment ratio of 1 indicates that there is one job opening for each unemployed person. Since the peak in the job openings rate in 2022, openings have steadily declined by nearly 3 percentage points while the unemployment rate has changed relatively little. The job openings-to-unemployment ratio has fallen from 2.06 to 1.12, indicating that for the moment, the job openings rate can fall (or in the case of this month, increase) without a commensurate adjustment in the unemployment rate.

Conclusion

As we wait for tomorrow’s employment report, the picture so far this year appears to be one of steady but slowing expansion. However, as much as hiring needed to moderate from its prior, unsustainable pace, further slowing would be worrisome. Certain industries bear close watching for signs of impending labor market weakness: durable goods; professional and business services; financial activities; leisure and hospitality; and information.

That said, we repeat a major caveat we wrote last month:

…developments in the labor market over the next year or so may be determined more by policy changes than by business cycle trends. For example, significant reductions in immigration flows could lead to reduced aggregate demand and thus reduced labor demand. The implementation of large, across-the-board tariffs would also reduce labor demand, particularly in the manufacturing sector. Such policy changes put at risk the soft landing, which otherwise appears well within reach.

Disruptive changes in fiscal policy could have outsized effects on the economy next year.

Acknowledgements

The authors thank Brad Hershbein for expert and helpful comments, Jimmy Zheng for material contributions to earlier versions of this work, and Olivia Howard, Noadia Steinmetz-Silber, and Joyce Chen for helpful research support.

Appendix